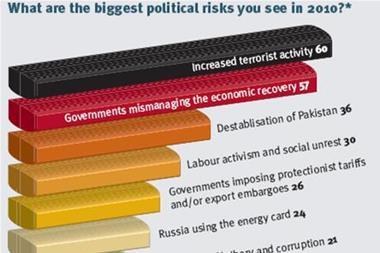

Are risk managers concerned about a potential rise in lawsuits, and can the D&O market remain stable? StrategicRISK, in association with ACE, surveyed you to find out

StrategicRISK’s latest reader poll reveals an increased emphasis on corporate governance and directors and officers (D&O) insurance in the wake of the financial crisis and ensuing corporate meltdowns.

A significant proportion (76%) of the 71 respondents said that the financial crisis had increased boardroom attention on executive liability issues and D&O insurance. Only 20% said it had not done so at all.

Even more worryingly, most of the respondents (80%) were concerned to some degree about executive liability lawsuits in their organisation. But only about one in 10 said this was “extremely concerning”.

Almost half of the respondents (46%) said that the financial crisis had significantly increased the emphasis on corporate governance in their organisation, while 44% said it had a little. Only 10% said there had been no effect. Shareholders have the biggest influence on corporate conduct, according to 32% of the respondents. A quarter (25%) of them stated that customers or consumers exerted the biggest influence.

A further quarter (25%) said that the government has the most influence over corporate behaviour. Only 8% thought that the media has the lion’s share of influence.

Organisations are mostly witnessing a backlash against their internal control and risk management systems as a result of the financial crisis, according to the survey respondents. Most of them also indicated that key stakeholders – such as shareholders, regulators, customers and the media – would push for more regulatory supervision, followed by a backlash against executive compensation, stricter corporate governance codes and higher ethical expectations. Senior management competence, non-executive oversight, proper accounting and reporting standards, and shareholder rights were also raised as areas of concern.

On the insurance side, over half (52%) of respondents said they had reviewed their D&O policy to ensure they have adequate protection. But all of these also thought that this review revealed that they did in fact have adequate protection in place. Almost a quarter (23%) have reviewed their policy and considered extending it in light of the financial crisis. A further quarter (25%) did not think it necessary to review their policy.

Asked about their concerns over the stability of the D&O insurance market in the future, the largest proportion of respondents (39%) were concerned that cover would be restricted or terms and conditions would harden unacceptably.

One in 10 respondents indicated they were worried that D&O insurers would slide into insolvency under the weight of claims. Almost a quarter (20%) said that they thought prices would increase significantly outside of the financial services sector, while 17% said they were worried about all of these issues. Only 14% were not concerned about any of these things happening.

Finally, respondents were evenly split about the stability of the D&O insurance market given the prospect of increasing executive liability claims. On balance, a small majority (52%) were confident that it would not face serious problems.

See the full results by downloading the PDF on the right of this page.

EXPERT VIEW

Current economic pressures are compelling companies to reduce their cost base, including insurance. But now is definitely not the time to "buy cheap" or to eliminate D&O.

At ACE, while we have yet to see any dramatic rise in D&O claims as a direct result of the financial crisis, we feel that companies need to appreciate more the multiplying influence of global governmental legislation and regulation on the liabilities of all managers, which is only partly precipitated by the economic crisis.

Looking ahead

It is increasingly difficult to say which actions taken by company leaders today have the potential for claims tomorrow. Most D&O is long-tail business, and can involve defence costs being met by insurers for years.

Now, more than ever, risk managers and financial officers need to buy responsibly, from insurers with a strong financial base, who underwrite responsibly, so they'll still be there when those future claims arise.

Don't buy cheap

Nevertheless, at ACE, while we believe some current rates cannot be sustained, we still observe new players coming into the market offering D&O as a loss leader.

The temptation for risk managers under fire to buy a policy offered as a bargain add-on to a standard property and casualty portfolio is real.

Buyer beware!

But beware: D&O is a unique, specialist cover and the quality of any policy needs to be examined carefully to ensure the terms protect at the right level and with the right breadth.

D&O needs to be a board concern. Experienced insurers handle D&O for companies and financial institutions separately, because of the very different needs of the sectors.

The voice of experience

Look at managing directors' and officers' risk more keenly as a better way to control current and future costs and there, too, experienced brokers and insurers with global credentials can really help.

Joe Fernandez, financial lines manager, Continental Europe, CIS and Russia, ACE Dan Holloway, UK and Ireland corporate financial lines underwriting manager, ACE

Downloads

Risk Register (see the full results here)

PDF, Size 0.64 mb

No comments yet