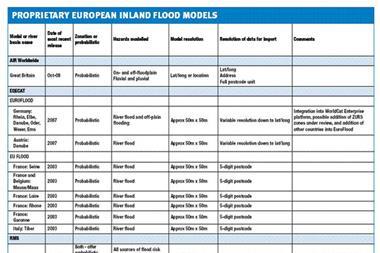

Modelling flood is a complex undertaking, owing to the numbers of variables that need taken into consideration, but the range of models is gradually growing which, together with improvements in mapping, will increase the confidence of insurers and reinsurers. By Rebecca Cheetham

Flood is a complex beast that can take on different forms. Within the insurance industry, the phenomenon of flood is commonly thought of in terms of river flooding, it being one of the main generators of insured losses for this peril, with the potential to affect several rivers and cause damage over a wide area. However, the term “flood” encapsulates a range of flood types, some of which are perhaps less well recognised, and these are summarised in Table1.

Modelling flood

Flooding in Europe is one of the major sources of natural catastrophe loss for the insurance and re-insurance industry. The use and continuing development of flood models will play an important role in a deeper understanding of the peril, which will allow decisions on all aspects of catastrophe assessment, management and compensation to be based upon scientific evidence. The majority of recently developed European flood models specialise in fluvial flood or storm surge, largely because these events are relatively common across Europe, or tend to occur on a sufficiently large scale to generate substantial insured losses.

Some other flood types, such as pluvial flood, have also been shown to generate considerable losses. For example, pluvial flood made a significant contribution to the June and July 2007 summer floods in the United Kingdom, which generated an estimated insured loss of 5.5 billion euros ($6 billion). Pluvial flood is more difficult to model due to the need for additional infrastructure data which may not be readily available. Nevertheless, models are now beginning to be developed that take account of it.

Modelling flood is a complex undertaking, owing to the numbers of variables that need to be taken into consideration. The hazard component of fluvial flood and storm surge models is physically based, meaning that the models are based on climatic and hydrological processes. The modelling of fluvial flood is particularly complex, demanding knowledge of the inter-relationships in the discharge of rivers in a particular drainage basin, in addition to information regarding defence structures and land topography.

The value of assets exposed to fluvial and coastal flooding is also projected to increase, because of rising trends in property value, increased development in high risk zones and in some cases, greater insurance penetration. Future trends in global climate change also indicate that precipitation across Europe may increase under the influence of a warming climate.

Flood model types

One accepted classification of flood models distinguishes between deterministic and probabilistic modelling processes. The deterministic model, in its purest form, consists of maps showing flood boundary limits for river discharge events of different return periods. This may also be termed a zonation model.

The calculation of a likely river discharge at different return periods (10, 15, 25, 50, 100 years, etc.) requires the historic river discharge data from gauge stations at intervals along the river section being modelled. Data from each gauge station are used to plot a curve of river discharge against the return period for which the historic data set allows.

For example, 50 years of historic discharge data can be used to give the river discharge of events of up to a 50 year return period. For the calculation of the discharge at return periods greater than 50 years, the plot of discharge against return period can be extrapolated to estimate the discharge of more extreme events, the accuracy of which increases in line with the amount of historic data.

Estimates of the discharge of different return period events at intervals along the river are used to model flood extent boundaries, which depend upon the topography of the floodplain. Topography information comes most commonly in the form of a digital terrain/elevation model (DTM or DEM). The accuracy of these data sets has a great impact upon the final quality of the flood maps.

Variations or extensions to a basic deterministic model can create models with greater sophistication. For example, river flood defences along the section of the modelled river can be taken into account on the basis of assumptions of their ability to withstand flooding from an event of a specified return period.

Models may also include estimates of the vulnerability of buildings on the floodable areas, which depends on the extent and depth of flooding. To do this requires additional knowledge of the built environment, such as building identity, age, location and construction material. With this information, it is possible to estimate not just which buildings would be affected by a specific event, but also the likely damage.

A probabilistic or stochastic model is a more complex way of representing real life situations. This modelling process introduces the possibility that there may be a number of results for a given situation. In this way, the model outputs can vary, given the same set of inputs.

In the production of a probabilistic flood model, the possibility of varying outcomes is introduced into certain components of the model. In this type of model, the hazard module includes a stochastic set of events, which gives a number of variables, typically water depth and flooded area, for each event in the set, based on river discharges, flood defence system characteristics and terrain data. Either river discharge or rainfall data can be used to create this set of events.

In the case of rainfall information, a hydrological component is used to transform precipitation data from different points during the synthetic events into net river discharge, which is then routed throughout the river network.

When the event set is based on discharge information, correlations are made between observed discharge data at the different gauge stations along the river network being modelled. These correlations give the extent to which the discharge between rivers in the drainage basin is related. They are then used to create a number of “synthetic” discharge possibilities from a single gauge station taken at random.

The final piece of a probabilistic model combines all model components to produce a number of flooding scenarios that can be run against a portfolio of risks to determine the material damage that each possible event would cause. A financial modelling component applies re/insurance information to produce the final loss exceedence curve, giving event return period against insured loss, specific to the portfolio.

Limitations to model accuracy

The accuracy of physically based flood models depends on the quality and availability of the data, as well as factors that are not considered during the modelling process that, nonetheless, have a large impact upon the consequences of a flood.

Input data

Every flood model incorporates a number of inputs and the quality of each affects the final results. The inclusion of information on river flood defences, obviously, has a large impact upon the final flooded areas modelled, but is not always possible because of restrictions on data use for commercial purposes. Even when data are available, there may not be adequate information on the structural integrity of defences, leading to an incorrect estimation of the level of protection actually provided.

Building vulnerability functions in the model influence how the flood intensity is translated into building damage. Vulnerability functions commonly use an engineering perspective, based on the knowledge that water depth and building type have the greatest effect on the overall amount of flood damage. These parameters by themselves over-simplify the quantification of flood damage, as claims experience shows that many other factors affect the total impact of a flood. These include flood duration, water velocity and debris load, the presence of chemical contaminants and human action. Although it would be too complex to take all these factors into account in the vulnerability curves, the final functions can be made more realistic by calibrating the output with insurance claims data.

The quality of digital terrain models can vary dramatically depending upon the methods used to create them, commonly remote sensing techniques, although direct land surveying or interpolation from topographic maps are also employed. Digital terrain model quality can be assessed in terms of how accurately the elevation is measured at each grid point covered by the model (vertical resolution) and the number of grid points at which elevation data is collected (horizontal resolution).

Variations in the vertical and horizontal terrain resolution are particularly important when modelling the water flow in flat valley bottoms, where changes in land gradient are gradual. The use of a more accurate digital terrain model will result in more accurate modelling of water flow and, therefore, in the location and extent of flooded areas.

Even when the best available data has been used in a model, the client’s own information can limit the accuracy of the model output if the data is incomplete or not at adequate resolution. This can apply where the client portfolio does not contain geocoded risk locations or the precise risk type. In such cases, the assumptions that will need to be made during the modelling process may not necessarily reflect reality.

Non-modelled components of flood loss

Flood mitigation schemes have a material impact on losses, but models rarely take them into account. It is possible, if not always easy, to model some protection measures, such as flood defences, but other schemes, such as flood preparedness education, are difficult to take into account, even though they have been shown to reduce individual losses, and can change quickly.

Business interruption is another aspect of loss that the majority of models find difficult to assess. Not only the direct effects offlood water on goods and business premises, but also damage to infrastructure, such as transport networks and power supplies, can have an impact on business.

Modelling the effects of flooding on business interruption would be desirable, but difficult to carry out on a country wide scale. For the immediate future, concrete improvements in flood model accuracy are likely come through investment in and the provision of more accurate datasets, and the modelling of certain aspects, such as pluvial flood, that have not, as yet, been commonly included in the development of fluvial flood models. Enhancement of our understanding of how human-induced climate change may affect future rainfall patterns and, therefore, flood events, will also play a central role in how the flood models of the future are developed.

Postscript

Rebecca Cheetham is part of Guy Carpenter’s European model development team. She is based in Paris. rebecca.cheetham@guycarp.com

www.guycarp.com

No comments yet