Nathan Skinner discusses findings from the latest analysis into the extent of economic and political risk

Recent analysis into the spread of political risk finds elevated risk in some of the world’s largest economies—but the picture is not all doom and gloom.

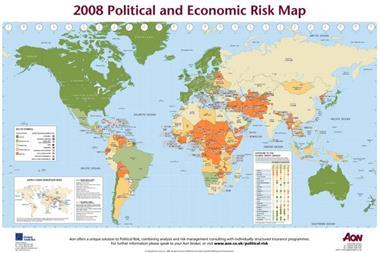

The release of Aon’s new Political and Economic risk map, comes just a few days after journalists penned their reactions to the World Economic Forum’s (WEF) Global Risks 2008 report.

Both studies share an interest in three key areas, supply chain risks, the global credit crunch and the role of energy.

The latest analysis found political and economic risk at its highest in the oil rich nations of Iran, Nigeria and Venezuela, where businesses face civil unrest, war, terrorism and non payment by governments for services rendered.

Meanwhile, only three countries received downgrades, Guinea-Bissau, Belarus and the Yemen, and the four major emerging markets—Brazil, Russia, India and China—are still characterised by a relatively benign risk environment.

Commenting on the results of the report Miles Johnstone, director of political risk at Aon’s Crisis Management said: ‘Overall, the trend towards improving stability around the world, as highlighted in previous years, has ended.’

A major concern for many is the supply of energy—the volatility of which was clearly demonstrated when Russia disrupted natural gas pipelines to Europe.

Energy risk is unlikely to abate any time soon, found the report, with most of the world’s oil reserves already in the hands of government-controlled companies and the signs of a protectionist backlash against foreign investment multiplying.

“Overall, the trend towards improving stability around the world, as highlighted in previous years, has ended.

Miles Johnstone, director of political risk

‘Pressure on nationalization of energy assets is driven by governments seeking to capitalise on high fuel prices,’ suggested Jens Tholstrup, executive director, Oxford Analytica, a partner in the research.

‘As the global demand for oil continues to grow in 2008, most of the demand will continue to be met by state owned companies,’ added the research.

Elsewhere in the analysis, concern was expressed about supply chain risks, particularly considering the world economies increased dependency on certain key resources moved along specific trade routes.

Recent supply chain events include, product safety recalls in China, transportation strikes in France and severe flooding in Bangladesh.

A new feature in this year’s analysis, the Credit Crunch Index, measured emerging markets exposure to international financial turmoil. While some commentators have found emerging markets to be more resilient to the credit crunch, the risk map authors claimed they are vulnerable. Latvia, Turkey, and Hungary topped the list of most exposed.

‘Countries that have boomed economically in recent years are now most at risk from the credit crunch,’ said Johnstone.

In a related finding, WEF expressed fears that the current liquidity crunch could spark a US recession in the next 12 months with the UK’s prominent financial sector making it ever more vulnerable. Aon placed the UK on Credit Risk Negative Watch due to its exposure to the sub-prime credit crunch.

This year’s risk map is the 15th and may go some way to explain the global risk management community’s heightened awareness of political instability. Nevertheless, worries about the threat that terrorism poses to business should be kept in proportion to the real risk, which is often miniscule.

No comments yet