FSCS reduction may be only temporary as brokers are urged to make provision for future levies

Brokers’ regulatory fees in the UK will fall by more than half this year thanks to the absence of a levy for the Financial Services Compensation Scheme (FSCS), according to a study by StrategicRISK’s sister title Insurance Times.

Although the reduction is good news for brokers, it is too soon to celebrate. The lack of the FSCS levy is likely to be a one-off, and there could be volatility in the FSCS charges in future years because of the way the fees are calculated and possible future mis-selling scandals.

Other fees have fallen in the past two years, but the Financial Conduct Authority (FCA) levy has been rising, which could be a concern for brokers.

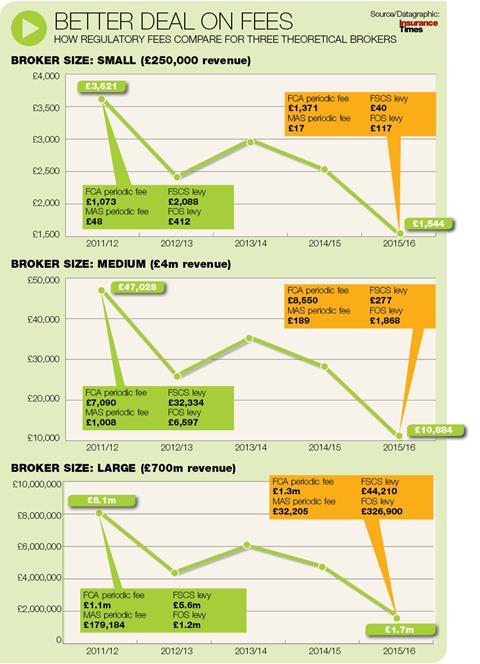

For the study, Insurance Times fed the revenue details for three theoretical brokers – one small, one medium and one large – into the online FCA fees calculator. The calculator enables users to check how much they will be charged by the FCA, FSCS, Money Advice Service and Financial Ombudsman Service.

The study found that the overall regulatory bill from the four bodies for brokers will more than half in 2015-16 on average for the three theoretical brokers.

Significant reduction

The biggest beneficiaries will be the largest brokers. The theoretical large broker used for the study, with annual revenue of £700m (€975.2m), will see its total regulatory fee package fall by 63.6% to £1.74m (€2.42m) in the year to 31 March 2016 from £4.79m (€6.66m) the previous year.

Small brokers will see a less dramatic but still significant reduction. A broker with an annual revenue of £250,000 (€374,359) will see total fees fall 39% to £1,544.73 (€2,146.31) from £2,534.16 (€3,521.16).

The biggest influence over the total is the FSCS charge. In 2014-15, it made up between 44% and 65% of the total fee package depending on the size of the broker.

However, for 2015-16, the FSCS fee will drop to between 2.5% and 2.6% of the total. The fall is so steep because brokers will not pay a key component of the FSCS charge in 2015-16. The FSCS pays consumers what they are owed by failed financial services firms if the firms cannot pay themselves.

The FSCS charge is made up of three parts: a base cost levy paid by all financial services firms, and two levies that are based on the category to which the company belongs. These cover the costs to the FSCS that are specific to that category, and also the costs of any compensation the FSCS has to pay out in relation to that category.

In 2015-16, brokers will pay only the base cost levy and will pay no charges related to their specific category.

Welcome news

This is because brokers already had a £19m (€26.4m) surplus from the year before, which more than covers the £17m (€23.62m) of category-specific compensation costs they were due to pay. The surplus was so high because compensation related to the payment protection insurance (PPI) mis-selling scandal has fallen faster than expected.

The news will be welcomed by brokers, not least because they objected strongly to paying high FSCS levies for a problem they did not cause.

Levies have been high because of the cost of paying out PPI compensation, and very few, if any, general insurance brokers sold PPI. They ended up paying because they are in the same fee category as the intermediaries that sold PPI and subsequently failed.

High regulation costs have long been a bone of contention among brokers as well as a staple of the British Insurance Brokers’ Association’s (BIBA) calls for more proportionate regulation. BIBA’s 2015 manifesto revealed that UK brokers’ direct cost of regulation, as a percentage of their income, was not only the highest in Europe but also higher than several other insurance hubs around the globe, including Singapore and Hong Kong.

The concern now is that brokers’ victory may be short-lived. Although they are falling, PPI claims have not gone away completely, and brokers perhaps should not expect a compensation levy of zero in future years.

Make provision

Compliance consultancy RWA’s compliance director Terence Clark said: “I would urge caution for next year.

“If brokers are looking to put budgets together for future years then make some provision for FSCS.”

Moreover, the figures for 2015-16 are still being consulted on and could change.

Furthermore, the way the FSCS now calculates levies means there is likely to be volatility in what brokers pay from year to year.

The scheme now calculates levies based on a three-year projection of compensation costs. The projections are based on historical costs, and so are tainted by the high PPI costs incurred in previous years.

BIBA head of compliance and training David Sparkes said: “This isn’t an appropriate way of charging the fees. Based on this three-year rolling plan, [the FSCS has] overcharged for what it needed and is now having to readjust it down to zero for this year.”

A further concern is that although other regulatory fees have been falling, the FCA annual fee has increased each year in the past three years. This will affect the smallest brokers hardest. In 2015-16, the theoretical small broker will pay 7.2% more than in 2014-15.

Sparkes says: “The FCA’s fees don’t correlate to the amount of activity that brokers do in a segment.

“So there is effectively a bit of cross-subsidising of the work the FCA is doing with banks in the figure that FCA are charging insurance brokers.”

No comments yet