In a hyper-connected and globalised world, businesses are increasingly at risk of disruption by major events on the other side of the world. But does traditional business interruption (BI) insurance respond in these scenarios?

From Icelandic volcanic eruptions grounding thousands of flights across Europe to floods in Thailand impacting the global demand for hard drive supplies, there are a growing number of examples of major natural catastrophes that have disrupted businesses and supply chains, often many hundreds of miles from where the actual event has occurred.

While affected businesses may not have experienced any direct physical damage to their premises, or even the property and premises of their major suppliers, their day-to-day activities are, nonetheless, disrupted.

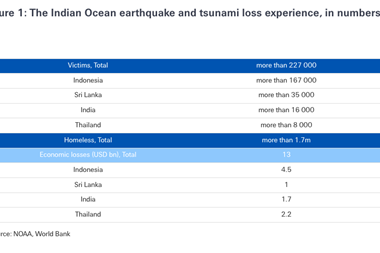

This was the situation for a flagship luxury store in Tokyo in the aftermath of the Tohoku Earthquake and Tsunami, which devastated the north east coast of the country in March 2011. The M9.1 quake claimed over 16,000 lives, destroyed hundreds of thousands of residential and commercial properties and caused widespread infrastructure damage. However, the premises of the luxury store emerged unscathed.

Following the catastrophe, it soon became apparent however that footfall had dramatically reduced and sales were suffering. “They thought it would be a case of going back to business as usual,” explains Jan Bachmann, senior structurer, Innovative Risk Solutions at Swiss Re Corporate Solutions. “And then six months later they realised there were fewer customers.”

“Customers had changed their behaviour, possibly because they needed to spend money on refurbishing their homes and recovering from the disaster, and they didn’t have as much money to spend on luxury goods.”

Too often, the losses that arise from this kind of disruption are not covered by traditional business interruption (BI) insurance. This is because most BI products focus on physical damage as a trigger for the policy to pay out. This means that while the luxury goods firm experienced a notable decline in business following Tohoku, its traditional BI policy would not indemnify it for those losses.

“We are living in a very complex world, in particular when it comes to natural catastrophes,” says Bachmann. “We find that many clients underestimate the complexity of major events. It’s not an easy task these days being a risk manager and having to assess this kind of exposure and determine risk transfer needs.”

He thinks parametric solutions, like the product designed for the Japanese luxury brand, is one way to tackle the ‘basis risk’ that can arise as a result of a major natural catastrophe. This is the risk that a company experiences a major loss, but that its insurance does not pay out.

Parametric insurance policies are triggered by an event of a certain magnitude with measurable, pre-agreed parameters, such as ground shaking or wind speed. Once the product is triggered it immediately pays out an agreed lump sum to the insured, regardless of whether or not the client has experienced any direct physical damage.

“With parametric we simply look at the magnitude of the quake, in this case, and we pay out a fixed pre-defined lump sum,” explains Bachmann. “We need some commitment and alignment of interests on the client side, but once we have this we can put together a parametric solution for business interruption.”

No comments yet